India

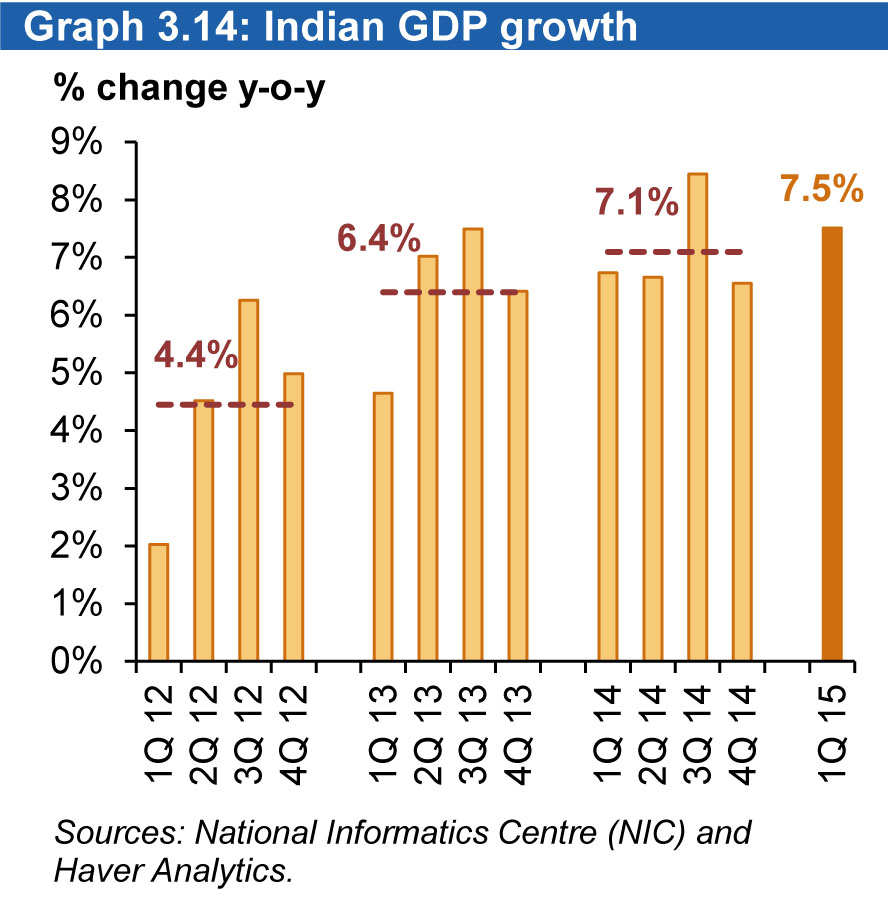

India’s economy grew 7.5% in the 1Q15, which was above expectations. It grew 7.3%

during the fiscal year ending 31 March. This means the country has outpaced China’s

economic expansion for two quarters out of the last three. It seems key positive

aspects are low commodities – and, specifically, low oil prices – which will limit the

current account deficit and lower inflation. Indeed, wholesale price inflation was

negative for the sixth consecutive month in April, while CPI inflation fell to a four-month

low. This will support consumers’ purchasing power and encourage spending.

When GDP components are investigated, on the demand side GDP has improved

visibly in January–March, while real private consumption spending grew 7.9% y-o-y,

the highest in seven quarters. Although this is in line with the notion of easing inflation

and lower interest rates supporting consumer spending (the CPI averaged 5.3% y-o-y

in January–March compared with 7.8% y-o-y during the same quarter last year), this

robust expansion contradicts much weaker data on consumer goods output,

particularly of consumer durables, which continued to contract in y-o-y terms. In the

meantime, real fixed investment grew 4.1% y-o-y, recovering from 2.4% y-o-y in the

4Q14 and bringing the annual average to 4.6%. Investment goods output expanded by

a respectable 9.6% y-o-y during the quarter and the imports of capital machinery grew

at double digits. The new investment announcements also increased 88% y-o-y during

the 1Q15. Despite the gradual improvement in demand-side GDP, the gross value

added data showed a steep decline in the 1Q to 6.1% y-o-y, bringing the annual

average to 7.2%. Here again, the government data showed a strong expansion in

manufacturing and financial and transport services, which grew 8.4% y-o-y, 10.2%

y-o-y and 14.1% y-o-y, respectively

The inflation rate in India was recorded at 4.87% in April of 2015. The CPI in India

increased to 120.7 index points in April 2015 from 120.2 index points in March. Since

the last RBI review in early April, oil prices have risen nearly 10% and the rupee has

depreciated nearly 3%. However, the baseline arguably had some associated

downside risks, and while the current move in oil prices and the value of the rupee are

likely to offset those risks and increase inflationary pressures, by themselves they are

unlikely to push inflation above the RBI’s 6% January 2016 target. Food inflation eased

to 6.14% in March from 6.88%, while the core part of the CPI remained largely sticky at

4.15% versus 4.10% in February. The prices of food and beverage items eased to

6.20% from 6.76%. The actual nature of the monsoons will be clear only around

mid-July. While a good monsoon can somewhat mitigate the impact of the unseasonal

summer rains on food prices, a bad one can do more damage. A much bigger worry is

a strong monsoon season that could drive up food prices. But there are mitigating

factors. The y-o-y deflation in WPI prices accelerated to 2.7% y-o-y in April from a 2.3%

rate in March. On a sequential basis, prices dropped for the seventh time in eight

months, declining by a seasonally adjusted (SA) rate of 0.5% m-o-m. The WPI has a

much larger tradable component than the CPI and, therefore, has been much more

responsive to the recent global commodity price fall. April was no different, with fuel

prices declining by a SA rate of 1.9% m-o-m on the back of pump price cuts at the end

of March. Furthermore, minerals prices declined by a SA rate of 0.8% m-o-m, reflecting

soft commodity prices. However, WPI deflation does not only reflect the first-round

impact of commodity prices. Falling input costs, weak domestic demand, and excess

capacity in key manufacturing sectors meant that core prices also declined sequentially

for the sixth straight month in April, falling by a SA rate of 0.2% m-o-m. As a

consequence, y-o-y core inflation remained unchanged in negative territory at -0.4%

y-o-y. India’s central bank cut its main interest rate by 0.25 basis points (bp) for the

third time this year, a move that appears at odds with recent data showing the country’s

economy has accelerated to become one of the fastest-growing in the world, with the

repo rate now at 7.25%.

Graph 3.16: Indian current account

Russia

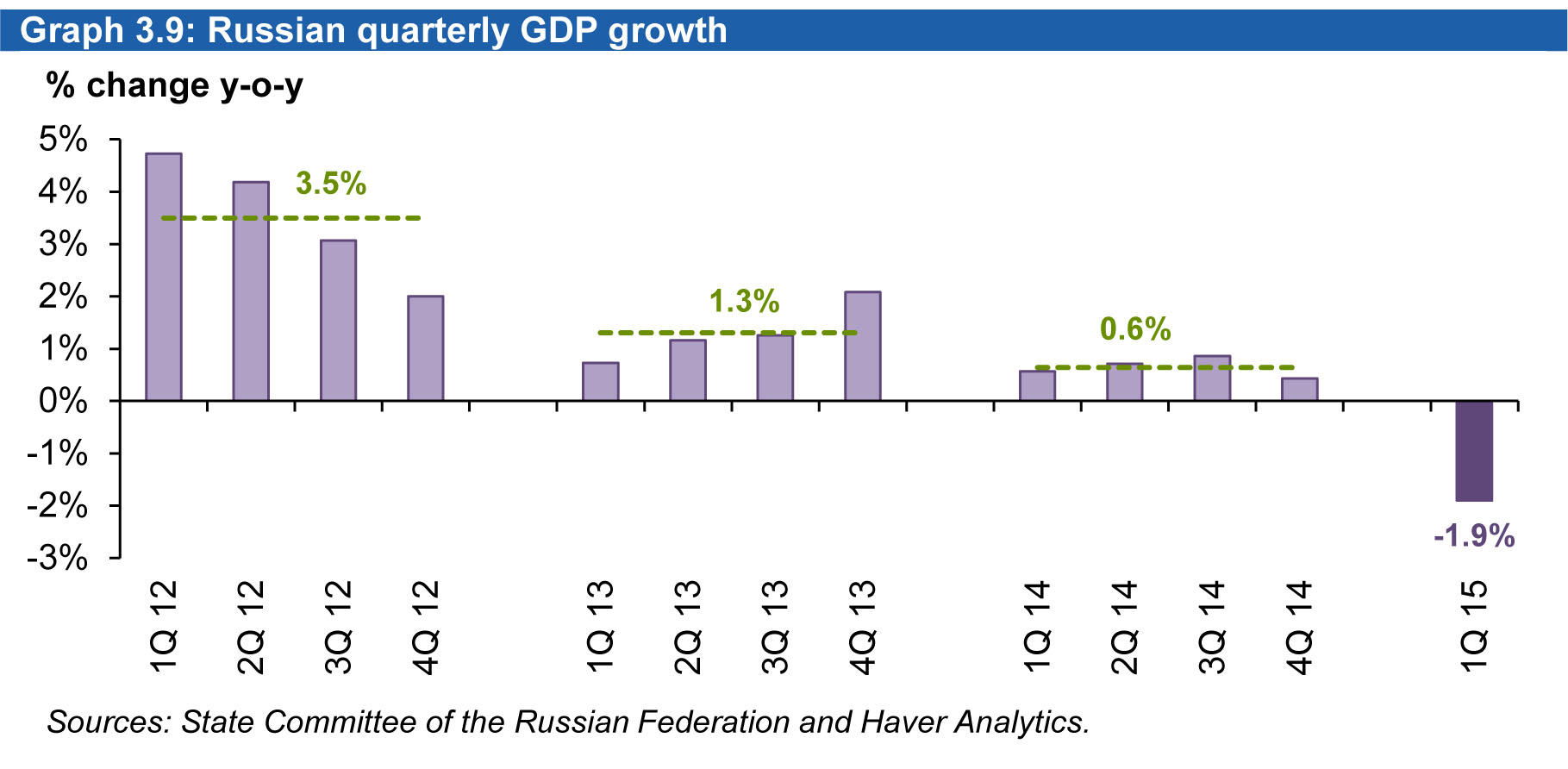

The GDP contracted 1.9% y-o-y in 1Q15, better than most expectations. Though

details about GDP components have not been released yet, data showed imports fell

by approximately 39% y-o-y in the same period, which is likely the reason behind the

better-than-expected

Inflation decreased to 15.8% y-o-y in May, easing slightly from 16.4% in April. In May,

the central bank reduced its benchmark interest rate to 12.5% from 14% in April.

Industrial production contracted 4.5% y-o-y in April, registering the third consecutive

deceleration. The drop in retail sales accelerated further in April, falling 9.8% y-o-y

from an 8.7% dip in March. Retail sales were in contraction for four months in a row

through April when they hit a record low reading. The unemployment rate in April

posted its first modest easing in seven months, standing at 5.8% in April from 5.9% a

month earlier. re.

Graph 3.9: Russian quarterl